Finance & Accounting

Finance & Accounting7 Accounting Best Practices For Businesses in 2026

January 21, 2026

|

Content

Efficient and effective accounting practices ensure compliance with regulatory requirements and provide critical insights into the financial health of a business. Whether you're a small startup or an established enterprise, implementing best practices in business accounting can help you make informed decisions, manage resources wisely, and drive long-term profitability.

However, navigating the complexities of business accounting can be daunting, especially with evolving regulations and the increasing demands of a competitive marketplace. Inaccurate or inefficient accounting practices can lead to financial discrepancies, missed opportunities, and even legal troubles.

To help businesses overcome these challenges and achieve financial excellence, this blog focuses on seven accounting best practices for businesses. By adopting these practices, you can address common accounting problems, enhance financial transparency, and make well-informed decisions that drive growth and profitability.

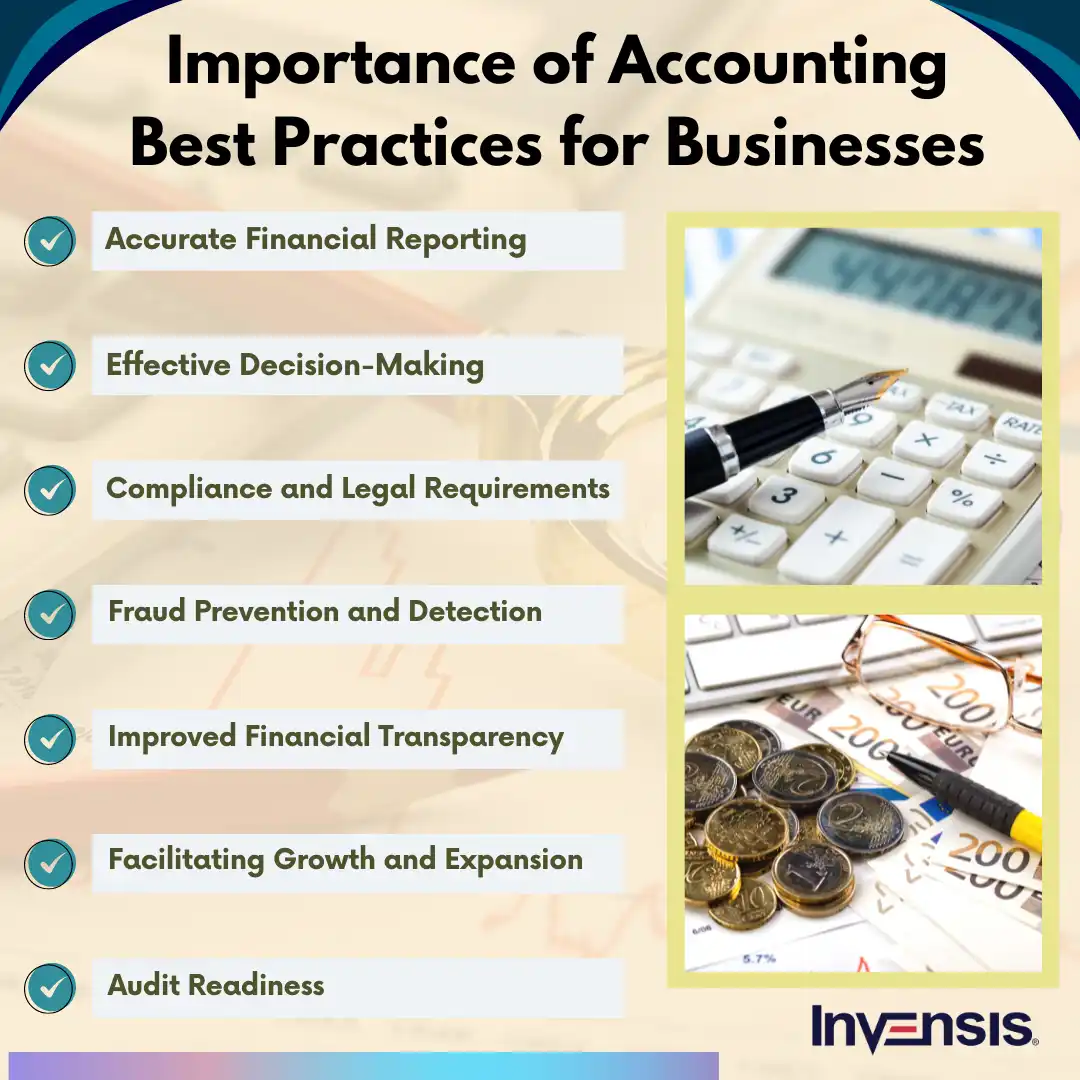

Importance of Accounting Best Practices for Businesses

Why Should Businesses Follow Accounting Best Practices in 2026?

Here are several reasons for businesses to follow effective practices in accounting 2026:

- Accuracy and Reliability: Best practices ensure accurate and reliable financial records, minimizing errors and discrepancies that can harm decision-making and stakeholder confidence.

- Regulatory Compliance: Adhering to accounting standards helps businesses meet legal and tax obligations, avoiding penalties, audits, or lawsuits.

- Enhanced Financial Transparency: Transparent reporting fosters trust among investors, creditors, and stakeholders, promoting long-term relationships and sustainable growth.

- Improved Decision-Making: Clear financial insights enable better strategic planning and resource allocation, supporting business growth and adaptability.

- Fraud Prevention: Best practices establish robust internal controls, reducing the risk of fraud, embezzlement, or financial misconduct.

- Cost Efficiency: Streamlined accounting processes optimize resource use, reduce operational costs, and improve overall business efficiency.

- Scalability and Growth: Proper accounting practices support scalability, making it easier to manage finances during business expansion or mergers.

Importance of Accounting Best Practices for Businesses

Best Practice 1: Implement a Robust Bookkeeping System

Accurate and organized bookkeeping is of utmost importance for businesses of all sizes. It is one of the accounting best practices that serve as the foundation for financial stability and informed decision-making. By meticulously recording and categorizing financial transactions, bookkeeping provides a clear picture of a company's income, expenses, and cash flow. This enables accurate financial reporting, allowing businesses to comply with legal and regulatory requirements. Moreover, organized bookkeeping facilitates effective tax planning and helps identify cost-saving and revenue growth areas. It also provides valuable insights into the financial health of a business, aiding in strategic planning and forecasting.

Consider a small retail store as an example. Proper bookkeeping lets the store owner track sales, inventory, and expenses effectively. However, the owner gains valuable insights by diligently recording each transaction, categorizing income and expenses, and maintaining an organized system. They can monitor the store's cash flow, identify top-selling products, track trends in customer spending, and evaluate profitability. This information empowers the owner to make informed decisions, such as adjusting pricing strategies, optimizing inventory levels, and identifying cost-saving opportunities.

Steps to Establish an Effective Bookkeeping System

Establishing an effective bookkeeping system is crucial for managing the financial records of a business or organization. Here are the steps to help you set up a solid bookkeeping system:

- Define your objectives: Determine the purpose and goals of your bookkeeping system based on your specific needs, such as tracking income and expenses or complying with tax regulations.

- Choose a method: Decide whether to use single-entry or double-entry bookkeeping, considering the size and complexity of your business.

- Set up a chart of accounts: Develop a categorized list of accounts that align with your business's financial transactions, such as assets, liabilities, equity, revenue, and expenses.

- Select bookkeeping software: Choose suitable software to streamline your record-keeping process, considering your business size, complexity, and budget.

- Record transactions: Enter all financial transactions accurately and categorize them properly in your bookkeeping system.

- Generate reports: Utilize your bookkeeping system to generate essential financial reports, such as balance sheets, income statements, and cash flow statements, to gain insights into your business's financial health.

Best Practice 2: Reconciling Accounts Regularly

Reconciling bank statements, credit card statements, and other financial accounts is an accounting best practice crucial to ensure accuracy and identify discrepancies. It helps verify that your bookkeeping records match the transactions and balances provided by the bank or credit card company. By reconciling regularly, you can detect errors, missing transactions, or potential fraud, enabling you to maintain accurate financial records, make informed decisions, and mitigate potential financial risks.

Let's consider an example to illustrate the importance of reconciling bank statements and credit card statements. Suppose your bank statement shows a deposit of $5,000, but your records indicate $4,500. Upon reconciliation, you discover a missing deposit of $500. By identifying and rectifying this discrepancy, you ensure accurate financial records. Similarly, reconciling credit card statements helps catch unauthorized charges or errors. For instance, if you notice a wrong charge during reconciliation, you can promptly address it with your credit card company.

How to Reconcile Accounts Effectively

Here is a step-by-step guide on how to reconcile your accounts effectively:

- Gather statements and records: Collect your bank statements, credit card statements, and other relevant financial records for the period you want to reconcile.

- Compare transactions: Take your bank statement and compare each transaction listed with your internal records. Check off each transaction as you verify it, ensuring that they match.

- Identify discrepancies: If you encounter any discrepancies, such as missing or incorrect transactions, note them separately for further investigation.

- Investigate discrepancies: Analyze the discrepancies by reviewing supporting documentation, such as receipts or invoices.

- Make adjustments: Once you have identified the cause of the discrepancies, make the necessary adjustments to your records. This could involve adding missing transactions, correcting errors, or removing duplicates.

- Reconcile ending balances: After making adjustments, ensure that the ending balance on your bank statement matches the balance in your records. This confirms that all transactions have been accounted for accurately.

Best Practice 3: Document and Organize

Documentation is a crucial accounting best practice as it provides evidence and support for financial transactions. It includes invoices, receipts, bank statements, contracts, and other relevant records. Proper documentation ensures transparency, accuracy, and legal and regulatory requirements compliance. It helps track and verify financial activities, facilitates auditing and tax filing processes, and provides a clear trail of financial transactions.

For example, a business receives an invoice for a purchase but fails to document it. Later, when reconciling accounts, they notice a discrepancy in their records. Verifying the transaction with proper documentation becomes easier, leading to clarity and potential financial inaccuracies. However, if the invoice had been properly documented, it would serve as evidence, enabling the business to accurately track expenses, reconcile accounts, and maintain a clear and reliable audit trail of their financial activities.

How to Organize Financial Documents

Here are the tips for organizing and storing financial documents:

- Use a filing system: Establish a consistent and organized filing system for your financial documents. Categorize them based on their type, such as invoices, receipts, bank statements, or tax records.

- Create subcategories: Within each category, create subcategories to organize your documents further.

- Maintain chronological order: Arrange your financial documents in chronological order to easily track the sequence of transactions. Label them with the date or use numeric naming conventions to ensure proper ordering.

- Digitize your documents: Consider scanning or digitizing your financial documents to reduce clutter and enhance accessibility.

- Backup your files: Implement a regular backup system for your digital financial documents. Create multiple copies and store them securely on external hard drives, cloud storage, or both.

- Establish retention periods: Understand the retention requirements for different types of financial documents based on legal and regulatory obligations. Create a document retention schedule to determine how long to keep each document type before securely disposing of them.

- Secure sensitive information: Safeguard sensitive financial information by implementing security measures. Use passwords for digital files, limit access to authorized personnel only, and consider encrypting sensitive data.

Best Practice 4: Segregate Financial Duties

Internal controls and the segregation of duties play a paramount role in business accounting. These accounting best practices safeguard a company's financial integrity and mitigate the risk of fraud or errors. Internal controls establish checks and balances, ensuring accurate recording, authorization, and asset safeguarding. Segregation of duties separates critical financial functions among different individuals, reducing the likelihood of collusion and increasing accountability.

Consider a scenario where a small manufacturing company implements internal controls and segregation of duties. The finance department ensures that only authorized individuals can access financial records, preventing unauthorized modifications or fraudulent activities. The responsibility for approving and disbursing payments is divided between employees, reducing embezzlement risk. This system not only safeguards the company's financial resources but also strengthens accountability and promotes a culture of transparency and trust within the organization.

How to Assign Responsibilities and Minimize Risks

Assigning responsibilities and minimizing the risk of fraud is crucial for maintaining the integrity of business operations. To achieve this, businesses should follow specific guidance:

- Segregation of duties: Assign different individuals to key financial tasks, such as record keeping, authorization, and reconciliation, reducing the risk of collusion.

- Clear job descriptions: Clearly define roles and responsibilities, ensuring employees understand their duties and are accountable for their actions.

- Regular oversight: Implement monitoring mechanisms to review financial activities, conduct internal audits, and spot any irregularities or suspicious transactions.

- Mandatory vacations: Require employees to take periodic time off, allowing others to step in and uncover fraudulent activities during their absence.

- Mandatory leave for key positions: Enforce mandatory leaves for employees in critical financial roles, enabling independent reviews and deterring long-term fraudulent schemes.

- Documented policies and procedures: Establish comprehensive policies and procedures for financial tasks, including proper authorization processes, expense approval limits, and documentation requirements.

- Training and awareness: Educate employees about fraud risks, detection techniques, and reporting procedures, fostering a culture of vigilance and accountability throughout the organization.

Best Practice 5: Conduct Regular Financial Analysis

Financial analysis is a crucial accounting best practice for informed business decision-making. It provides insights into financial performance, profitability, liquidity, and solvency. By evaluating trends, ratios, and statements, businesses can identify strengths, weaknesses, and areas for improvement. This analysis helps with cost control, pricing strategies, resource allocation, and assessing project viability. It enables decision-makers to understand the impact of choices on cash flow and overall financial health. With quantitative data, businesses can make strategic decisions, leading to improved financial outcomes and long-term success.

For instance, consider a manufacturing company analyzing its financial statements and ratios. Through financial analysis, they discover that their inventory turnover ratio has decreased, indicating slow-moving inventory. This prompts the company to reassess its production processes, adjust inventory levels, and implement more efficient supply chain management strategies. By leveraging financial analysis, businesses can make informed decisions that optimize operations, reduce costs, and enhance profitability, ensuring long-term success in a competitive market.

How to Perform Financial Analysis Effectively

Performing financial analysis effectively requires the use of various techniques. Here are some techniques to consider:

- Ratio Analysis: Calculate and analyze financial ratios such as liquidity, profitability, and efficiency. These ratios provide insights into a company's financial performance and help assess its strengths and weaknesses.

- Trend Analysis: Examine financial data over multiple periods to identify trends and patterns. This helps understand the direction and magnitude of changes in key financial indicators, enabling better forecasting and decision-making.

- Comparative Analysis: Compare the company's financial data with industry peers or competitors. This benchmarking allows for a better understanding of the company's performance relative to others in the same market, highlighting areas for improvement or competitive advantages.

- Cash Flow Analysis: Analyze cash inflows and outflows to assess the company's ability to generate and manage cash. This analysis helps identify cash flow patterns, liquidity risks, and areas where cash can be better allocated.

- Break-Even Analysis: Determine the point at which revenue equals expenses to assess the level of sales or production needed for profitability. This analysis helps understand cost structures, pricing strategies, and the impact of changes in volume or costs.

- Sensitivity Analysis: Evaluate the impact of different scenarios and variables on financial outcomes. Businesses can assess the potential risks and opportunities associated with different scenarios by modeling changes in factors like sales, costs, or interest rates.

- Financial Forecasting: Use historical data and trends to project future financial performance. Forecasting allows businesses to anticipate potential challenges, plan for growth, and make informed decisions based on predicted outcomes.

Best Practice 6: Comply With Tax Regulations

Businesses have various tax obligations that must be fulfilled. These include income tax, where businesses are required to report their revenue and calculate their taxable income. Additionally, businesses are often responsible for collecting and remitting sales tax on goods and services sold. Payroll taxes must be deducted from employee wages and paid to the appropriate tax authorities. Failure to meet these tax obligations can result in penalties and legal consequences, making tax compliance a crucial aspect of business operations.

Let's consider a manufacturing company. To meet its tax obligations, the company must accurately report its annual revenue, deduct allowable expenses, and calculate its taxable income. It is also responsible for collecting and remitting sales tax on customer products. Additionally, the company must withhold payroll taxes from employee wages and submit them to the relevant tax authorities. Complying with these tax obligations is essential to avoid penalties and legal issues.

How to Comply and Minimize Tax Liabilities

Here are some tips for ensuring compliance and minimizing tax liabilities:

- Stay updated on tax laws: Keep abreast of changes in tax laws and regulations relevant to your business. This helps you understand your obligations and take advantage of tax incentives or credits.

- Maintain accurate records: Maintain organized and up-to-date financial records, including receipts, invoices, and expense documentation. This ensures you have the documentation to support deductions, credits, and exemptions.

- Consult with a tax professional: Consider working with a tax professional or accountant specializing in business taxes. They can provide guidance, help you identify potential deductions, and ensure compliance with tax laws.

- Plan and strategize: Develop a tax planning strategy that aligns with your business goals. This may involve timing income and expenses, making strategic investments, or considering entity structure options to optimize your tax position.

- Utilize deductions and credits: Familiarize yourself with your business's eligible deductions and tax credits. Take advantage of available deductions such as business expenses, depreciation, and research and development credits to reduce your tax liability.

- Monitor tax deadlines: Stay aware of tax filing deadlines to avoid penalties or late fees. Set reminders and establish a system to ensure timely submission of tax returns, payments, and necessary documentation.

- Seek professional advice for complex matters: Consider consulting a tax professional for complex tax matters or significant transactions. They can provide expert guidance and help navigate complex tax issues, reducing the risk of errors and non-compliance.

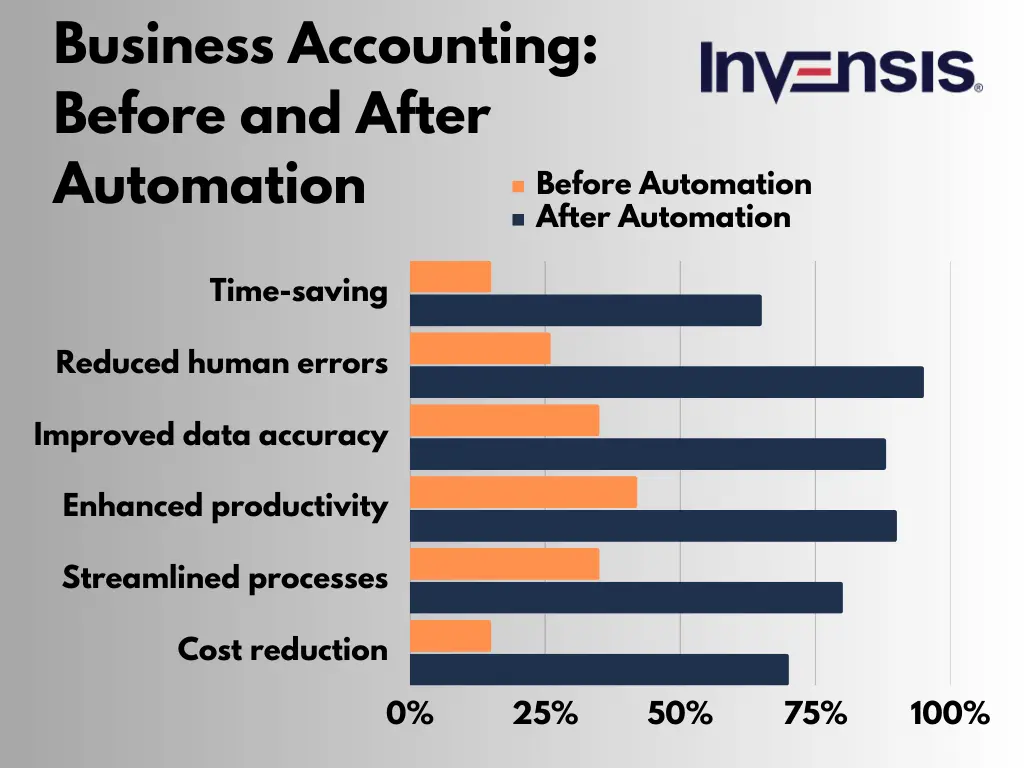

Best Practice 7: Utilize Accounting Software and Automation

Using accounting software offers numerous advantages for businesses as it is one of the main accounting best practices. It streamlines financial processes, automates calculations, and reduces the likelihood of manual errors. Accounting software provides real-time access to financial data, enabling better decision-making and financial analysis. It simplifies invoicing, expense tracking, and reconciliation, saving time and improving efficiency. Additionally, software-generated reports and analytics facilitate compliance with tax regulations and aid audit preparation.

For example, a construction company that traditionally managed its finances manually transitioned to accounting software. The software automated tasks like payroll processing, expense tracking, and invoicing. This eliminated the need for time-consuming manual calculations and reduced the risk of errors. Additionally, the software provided real-time insights into project costs, profitability, and cash flow, allowing for better financial decision-making.

How to Choose the Right Software

When choosing accounting software and leveraging automation, consider the following recommendations:

- Assess your business needs: Evaluate your specific accounting requirements, and consider factors like the size of your business, industry-specific needs, scalability, and integration with other software or systems.

- Research available options: Explore different accounting software solutions in the market, read reviews, and compare features, pricing, and customer support. Look for software that aligns with your needs and offers user-friendly interfaces.

- Consider cloud-based solutions: Cloud-based accounting software provides flexibility and accessibility from anywhere with an internet connection. It also offers automatic software updates and data backup, reducing the burden on your IT infrastructure.

- Evaluate automation features: Look for software with robust automation capabilities, such as automated bank feeds, recurring invoicing, expense categorization, and financial report generation.

- Scalability and future growth: Choose software to accommodate your business's growth and evolving needs. Consider its ability to handle increased transaction volumes, multi-currency support, and advanced reporting features.

- Security and data protection: Ensure the software provider prioritizes data security and has appropriate measures, such as encryption, secure data storage, and regular backups. Understand their privacy policy and compliance with data protection regulations.

- Training and support: Consider the availability of training resources, user guides, and customer support provided by the software vendor. Adequate training and reliable support can maximize the benefits of the software and address any issues or questions that may arise.

Conclusion

The future of business accounting holds immense potential, driven by technological advancements and evolving industry practices. Businesses must adapt to these trends and changes to stay competitive and thrive in the dynamic landscape. The rise of automation, artificial intelligence, and cloud-based solutions will revolutionize accounting processes, enabling businesses to streamline operations, reduce manual errors, and improve efficiency. But, implementing these advancements in real-time business becomes a challenging task. Businesses must involve continuous learning and upskilling to stay abreast of technological advancements in the accounting field. An expert business accounting firm like Invensis can pull you out of this challenge.

Invensis offers the right accounting tools, expertise, and resources to handle your complex accounting needs. With our assistance in bookkeeping services, businesses can manage their finances effectively, resulting in revenue growth, financial stability, and steady cash flow. Contact us today to regularize your financial operations for growth enhancement!

.webp "Medium")

Rick is a highly accomplished finance and accounting professional with over a decade of experience. Specializing in delivering exceptional value to businesses, Rick navigates the complexities of the financial realm easily. His expertise spans various industries, consistently providing accurate insights and recommendations to support informed decision-making. Rick simplifies complex financial concepts into actionable plans, fostering collaboration between finance and other departments. With a proven track record, Rick is a leading writer who brings clarity and directness to finance and accounting, helping businesses confidently achieve their goals.

Discover Our Full Range of Services

Click HereExplore the Industries We Serve

Click HereBlog Category

Related Articles

How quickly they turn invoices into cash, we break down what really happens inside the invoice validation clock

June 25, 2026

|

A practical guide for factors to identify invoice fraud, strengthen invoice validation, and protect funding decisions.

June 25, 2026

|

.jpeg)

How modern factoring support services empower factoring companies to scale, manage risk, and protect margins amid tightening credit conditions.

June 25, 2026

|

Services We Provide

Industries We Serve