Finance & Accounting

Finance & AccountingWhat is Project Accounting? A Complete Guide

September 30, 2025

|

Content

Project accounting is the discipline that brings financial precision by managing each project as its own business. Unlike traditional accounting, which reports at the organizational level, project accounting isolates budgets, revenues, costs, and risks at the project level, delivering insights that broader financial systems cannot.

The importance of this approach is underscored by research indicating that nearly 70% of projects fail to meet their original objectives or budgets. In such an environment, financial clarity becomes not a support function, but a decisive factor between delivering measurable value and absorbing costly overruns.

Oliver F. Lehmann, an authority on project business management, captures this risk clearly:

Managers, including project managers, prefer to base decisions on numbers. Give them wrong numbers and they will make poor decisions.

- PM World Journal

His insight underscores the stakes. Without accurate project-level tracking, organizations operate without a compass, exposing themselves to budget overruns, misallocated resources, and eroded stakeholder trust. Project accounting fills that gap, providing the reliable numbers leaders need to steer projects to success.

In this guide, we define project accounting, highlight its importance, outline its guiding principles, and show how organizations can put it into practice

Let’s dive in.

What is Project Accounting?

Project accounting is a type of managerial accounting that is specifically designed for the duration of a project. Project accounting tracks budgets, revenues, costs, assets, liabilities, and performance metrics on a per-project basis, treating each project as its financial universe.

Project managers play a crucial role in project accounting. They are responsible for overseeing the economic aspects of the project and ensuring that it stays within budget and meets its financial goals, unlike standard accounting, which views a firm as a single, large entity.

In practice, it tracks:

- Project budgets (planned vs. actual costs).

- Revenues tied to deliverables or milestones.

- Labor hours and resource costs.

- Materials, licensing, and overheads.

- Profitability and return on investment.

For example, while traditional accounting might report that a company spent $2 million on “operations” in Q2, project accounting drills down to say:

- $500,000 went to Project A (construction).

- $700,000 to Project B (IT system rollout).

- $800,000 to Project C (marketing campaign).

It is simpler to determine which initiatives are lucrative, which are overpaying, and where remedial action is required when there is this degree of visibility.

As Peter Drucker said:

“You can’t manage what you can’t measure.”

- Peter Drucker

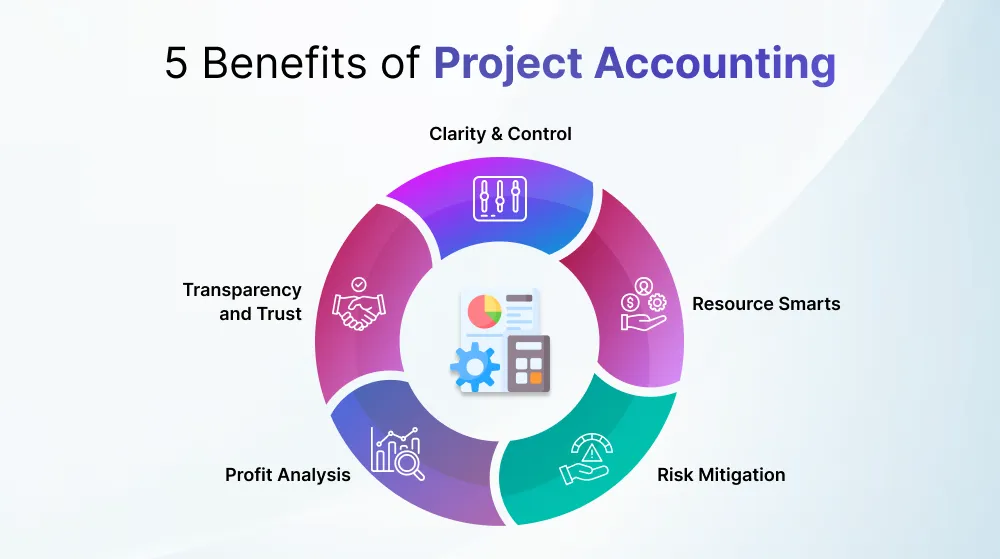

5 Benefits of Project Accounting

Projects are intricate financial ecosystems with moving components, varying deadlines, and changing scopes; they are not simply “tasks.” Some are so large, such as defense contracts, hospital construction, or multibillion-dollar highway projects, that even the most minor error can have repercussions on communities, stakeholders, and national budgets.

Project accounting is invaluable for large-scale, complex projects where financial stakes are high and errors can be costly. However, it’s equally critical for small and mid-sized businesses, where budgets are tighter, resources are limited, and a single miscalculation can have a disproportionately negative impact on overall profitability. It’s a strategic need rather than a luxury. Let’s examine why it is essential:

1. Clarity & Control

The discrepancy between what is planned and what is occurring on the ground is one of the most challenging problems in project management. This gap is filled by project accounting, which offers real-time insight into financial performance.

Project accounting instantly raises a red flag, for instance, if a building project budgeted $500,000 for supplies but real spending has already reached $450,000 halfway through. This enables managers to make early course corrections through contract renegotiation, schedule modifications, or resource reallocation.

Structured project accounting, as per Deltek, empowers managers with enhanced cost visibility and control through detailed job cost reports and insights into resource burdens. This early detection of overruns enables corrective action to be taken before budgets spiral out of control, instilling confidence and capability in managers.

2. Resource Smarts

The effective management of resources, including personnel, time, tools, equipment, licenses, and administrative costs, determines whether a project succeeds or fails. Organizations can monitor these in-depth through project accounting to ensure they’re being used effectively.

The system alerts users, for example, when a software license is not being utilized to its full potential or when a department records an excessive number of labor hours compared to the budget. By optimizing utilization, businesses avoid waste and maintain staff productivity.

This approach focuses on managing resources effectively, not just people, but also time, tools, equipment, licenses, and administrative costs. It minimizes resource conflicts through techniques such as time tracking, scenario planning, and workforce optimization, ensuring that resources are utilized efficiently and that projects are delivered on time and within budget.

3. Risk Mitigation

Project accounting is proactive in risk mitigation because it ties financial data directly to specific project phases, something traditional accounting does not. It identifies potential issues early, like scope creep, delays, or overspending, before they escalate.

This unique linkage between project milestones and financial performance provides managers with real-time visibility, reducing the need for reactive measures and enhancing their sense of control.

4. Profit Analysis

Project accounting is about learning as much as it is about spending management. Organizations can determine what caused losses and where revenues came from by gathering post-project insights.

For instance, a software company may discover that, despite higher hourly rates, local hires performed better on projects where it used offshore engineers. In contrast, the latter had lower profits because of hidden training costs. Future bidding tactics are shaped by these findings, which enable companies to pursue only profitable contracts.

Glasscubes integrates project management and accounting practices, reports a 33% increase in projects delivered under budget, and a 25% reduction in unsuccessful efforts.

5. Transparency and Trust

Stakeholders, investors, and clients are calling for more thorough financial disclosure. Vague phrases like “we’re on track” are not what anyone wants. They want concrete figures, such as revenue projections, burn rates, and remaining budgets.

That is precisely what project accounting offers. It gives stakeholders confidence that the project is in capable hands by producing reports, dashboards, and KPIs that are simple to read. This type of transparency isn’t discretionary for businesses involved in government contracts, construction, and IT consulting; in fact, it’s frequently mandated by law or regulation.

According to PMI’s Pulse of the Profession, two in five projects fail to meet their original goals. Of those, one-half of all projects fail due to ineffective communication and reporting. Implementing transparent project accounting directly addresses this gap, making organizations more trustworthy and competitive.

How Project Accounting Works

Project accounting provides a structured approach to plan, monitor, and control financial activities throughout a project’s life cycle. Unlike general accounting, which looks at the organization as a whole, project accounting focuses on a single project, breaking down revenues and expenses at a detailed level.

1. Budgeting

The process begins with budgeting. A cost plan is developed to estimate expenses, including labor, materials, equipment, and overhead. This budget becomes the benchmark against which all project costs are measured.

2. Track Actual Costs Against Planned Costs

Once the project starts, project accountants and managers continuously track actual costs against planned costs. This variance analysis helps determine whether spending is on track, over budget, or under budget, enabling timely corrective actions.

3. Documentation

Every expense must be accurately recorded, from contractor payments to resource usage, to create a transparent financial trail. This is critical for compliance, audits, and decision-making.

4. Future-based costs

Project accounting also accounts for future-based costs, such as upcoming payments tied to legal agreements, contracted delivery schedules, and anticipated completion expenses. Additionally, it tracks revenues generated from project-specific contracts, ensuring that profitability can be accurately measured and reported.

8 Core Principles of Project Accounting

While understanding how project accounting works provides a comprehensive view, the framework is guided by eight key principles that ensure accuracy, transparency, and financial control throughout the project lifecycle.

Here are the eight key accounting principles:

8 Steps to Implement Project Accounting Successfully

Step 1: Define Clear Objectives

Start by asking yourself and your leadership team: “Why are we doing project accounting?” Without a clear purpose, the process becomes another layer of admin.

For example, a construction firm might answer: “We want to track whether our roofing project is profitable on its own, not just as part of company-wide revenue.” A marketing agency might say: “We need visibility into campaign-level costs and margins.”

Write down 2–3 measurable goals. For instance:

- “Reduce project cost overruns by 10% this year.”

- “Provide monthly profitability reports at the project level.”

- “Improve client transparency with monthly cost reports.”

These goals will serve as the benchmark when you evaluate whether project accounting is working.

Step 2: Develop Detailed Budgets

Before starting the project, create a budget breakdown. This prevents surprises mid-way.

For example, in Excel or project accounting software, create columns for:

- Labor (e.g., 200 hours × $50/hr = $10,000)

- Materials (e.g., licenses = $1,500)

- Subcontractors (e.g., consultant = $2,000)

- Overheads (e.g., utilities = $500)

A $50,000 marketing campaign budget might look like:

- Ads: $25,000

- Design: $10,000

- Staff time: $10,000

- Reporting tools: $5,000

Share this budget with your team so everyone knows the limits before the project starts.

Step 3: Set Up Project Subledgers

Now you need a place where every transaction for each project is recorded. In most accounting systems, this means creating separate project accounts or cost centers.

If you’re using QuickBooks:

- Go to Chart of Accounts.

- Click New Account.

- Name it something like “Project A – Website Build.”

- Assign it as an Income/Expense account.

From now on:

- Any invoice to Client A goes under this account.

- Any labor hours, materials, or subcontractor costs go here too.

At month-end, you can pull a Profit & Loss report specifically for Project A, instead of looking at only company-wide numbers. This makes project-level profitability instantly visible.

Step 4: Implement Controls and Approval Workflows

Next, put guardrails in place. Decide on spending limits that require approval.

For example:

- Rule: “Any expense above $1,000 must be approved by the Finance Manager.”

If a project manager wants to hire a freelancer for $1,200, they submit the request for approval. This prevents “surprise expenses” from appearing later.

Most accounting tools (QuickBooks, SAP, NetSuite) allow you to set automated approval rules. If not, create a simple email approval chain.

This step protects project profitability by stopping uncontrolled spending.

Step 5: Use the Right Revenue Recognition Method

One of the biggest challenges in project accounting is: “When should we recognize revenue?”

- For long-term projects (e.g., construction over 12 months), use the Percentage of Completion method. If you finish 40% of a $100,000 project, recognize $40,000 revenue.

- For short-term jobs (e.g., a 1-week training workshop), use the Completed Contract method. Recognize revenue only when the project is fully delivered and signed off.

Using the right recognition method ensures your books reflect reality and prevents overstatement of revenue.

Step 6: Integrate with Core Systems

Project accounting works best when it’s connected to your ERP or core accounting software.

For example, in NetSuite or QuickBooks with add-ons:

- When payroll is processed, hours logged on “Project A” automatically show up in that project’s ledger.

- When expenses are submitted, they sync directly to the correct project account.

This eliminates manual data entry and ensures every cost is captured in the right place, in real time.

Step 7: Provide Regular Reporting

Set a routine for project financial reporting. Weekly or biweekly works best.

Reports should show:

- Budget vs. Actual Spend.

- % of work completed vs. % of budget used.

- Profit margin to date.

Example: “Project A is 60% complete but has already used 75% of its budget risk of overspending.”

With this visibility, managers can act early instead of reacting when the project is already off track.

Step 8: Train Your Teams

Even the best system fails if people don’t know how to use it. Run a training session (1–2 hours) for project managers, accountants, and team members.

Show them:

- How to log time against a project.

- How to request approval for an expense.

- How to generate a simple project-level report.

Provide cheat sheets or short video tutorials for new hires so the process sticks.

Training ensures consistency. Everyone records costs and revenues the same way, so reports remain reliable.

5 Project Accounting Revenue Recognition Methods

Revenue recognition in project accounting is crucial because it determines when income from a project should be recorded in financial statements. Since projects often span months or even years, choosing the correct method ensures compliance, accuracy, and transparency in financial reporting. Here are the primary methods used:

Percentage-of-Completion (PoC) Method

- Revenue is recognized gradually in proportion to the work that has been completed.

- Typically calculated using either cost-to-cost (costs incurred vs. total estimated costs) or efforts-expended (hours worked vs. total estimated hours).

- Best suited for long-term projects where progress can be reliably measured.

- Benefits: Provides steady revenue recognition and reflects actual progress.

- Risk: Requires accurate forecasting of costs and timelines.

Completed-Contract Method

- Revenue is only recognized when the project is fully completed and delivered.

- Suitable for short-term projects or when project outcomes are uncertain.

- Benefits: Reduces the risk of recognizing revenue prematurely.

- Risk: May cause significant fluctuations in financial results, as all revenue and profit are recorded simultaneously.

Milestone Method

- Revenue is recognized when specific, measurable project milestones are achieved.

- Common in industries like software development, R&D, and construction.

- Benefits: Ties revenue recognition to tangible deliverables, increasing transparency.

- Risk: Defining and agreeing on milestones can be a complex process.

Cost-Recovery Method

- Revenue is recognized only when project costs have been fully recovered.

- Used in high-risk projects where profitability is uncertain.

- Benefits: Very conservative approach; ensures no revenue is overstated.

- Risk: Delays recognition of profit, which may understate performance in the short term.

Installment Method

- Revenue is recognized as payments are received from the client.

- Common in projects with extended payment schedules or financing arrangements.

- Benefits: Reduces credit risk since revenue is only recognized when cash is collected.

- Risk: May not reflect the actual progress of the project.

5 Project Accounting Best Practices

Implementing project accounting successfully hinges not just on tracking numbers but on adopting practices that ensure accuracy, adaptability, and transparency. Below are key best practices:

1. Maintain a Separate, Granular System for Project Accounting

Rather than using your general ledger, establish a dedicated accounting system or detailed project subledgers that capture all project-specific transactions, including both costs and revenues. This ensures every financial event is tied to the right project, which improves visibility and accountability.

Babcock & Wilcox (B&W), a major power-generation firm, integrated Oracle Primavera P6 with its SAP ERP and used EcoSys EPC as a bridge. This enabled detailed project-level cost controls, automated earned-value metrics, and accurate client and internal reporting.

2. Increase Reporting Frequency Near Critical Milestones

Move beyond monthly or quarterly reporting. As a project nears critical milestones or its end date, reports should shift to a weekly or even daily cadence. This ensures that emerging issues are identified and addressed in real-time.

NASA’s Mars 2020 mission (Perseverance rover) followed strict Earned Value Management practices. During high-risk phases including testing and launch they closely monitored progress and costs, enabling quick course-corrections.

3. Simplify Reports Around Project KPIs

Tailor your reports and dashboards to each project’s key performance indicators (KPIs). Use visual cues, such as color-coded alerts for budget variances, so decision-makers can immediately see when adjustments are needed.

A global construction firm modernized its operational reporting by integrating Knowledge Relay with Primavera P6. Users now get real-time, multi-source dashboards that drive faster, data-informed decisions.

4. Regularly Update Budgets and Forecasts

Project accounting isn’t static. Continuously forecast upcoming costs and update your budget accordingly. This proactive approach enables better cash flow planning and keeps stakeholders aligned with realistic, up-to-date projections.

Technip, a global oil & gas contractor, standardized its forecasting across currencies and cost categories. Using EcoSys EPC, they tracked multiple budget versions side-by-side, enabling timely and more accurate margin analyses.

5. Track Resources with Precision

Monitor labor, materials, and third-party costs carefully, especially in time-and-materials (T&M) projects. Monitor labor hours, potential overages, and material delivery delays to identify issues before they escalate.

ValleyCrest (a national landscaping company) integrated Oracle’s Contract Management with EnterpriseOne. Their nightly data sync ensured that invoice, cost, and billing data are aligned per project, eliminating duplication and improving accuracy.

Simplify Your Project Accounting with Invensis

Project accounting doesn’t have to be complicated. From tracking costs to recognizing revenue, automation is the key to saving time, reducing errors, and ensuring compliance. Invensis provides end-to-end project accounting outsourcing solutions that streamline your processes, improve financial accuracy, and free your team to focus on growth.

Conclusion

In projects where timelines, budgets, and deliverables intersect tightly, financial clarity isn’t optional; it’s essential. Project accounting transforms chaos into clarity. It enables more intelligent decision-making, improves profitability, reduces risk, and builds stakeholder trust.

Whether you’re a small consultancy managing client engagements or a global construction firm building infrastructure, embedding sound project accounting practices and leveraging modern software tools can mean the difference between thriving and barely surviving.

Frequently Asked Questions

.webp "Medium")

Ryan is a seasoned professional in the back office arena, bringing extensive knowledge and expertise to the table. With years of experience, he effortlessly manages the intricacies of back office operations. Ryan's proficiency spans diverse industries, consistently providing valuable insights and efficient solutions. He excels in streamlining processes, promoting seamless collaboration, and optimizing productivity. As a prominent writer in the back office domain, Ryan delivers concise and practical advice, empowering businesses to thrive efficiently.

Discover Our Full Range of Services

Click HereExplore the Industries We Serve

Click HereBlog Category

Related Articles

How quickly they turn invoices into cash, we break down what really happens inside the invoice validation clock

June 25, 2026

|

A practical guide for factors to identify invoice fraud, strengthen invoice validation, and protect funding decisions.

June 25, 2026

|

.jpeg)

How modern factoring support services empower factoring companies to scale, manage risk, and protect margins amid tightening credit conditions.

June 25, 2026

|

Services We Provide

Industries We Serve